Cash Flow Management for Small Businesses

Last Updated: June 12, 2026

Cash flow management is the most important financial skill to master in a small business because cash flow determines whether you make it through your first five years or establish a long-term road to success. Eighty-two per cent of small businesses that fail despite being profitable say the cause was cash flow. This is not about bad products or soft demand. This is about timing: the money that is due not coming when you need it to pay the money that is due.

Come 2026, Indian SME businesses may be burdened with 10.7 lakh crore of receivables, and 71% might have to source additional capital just to sustain their daily operations. It is therefore imperative for small businesses to learn how cash flows work.

What is Cash Flow Management?

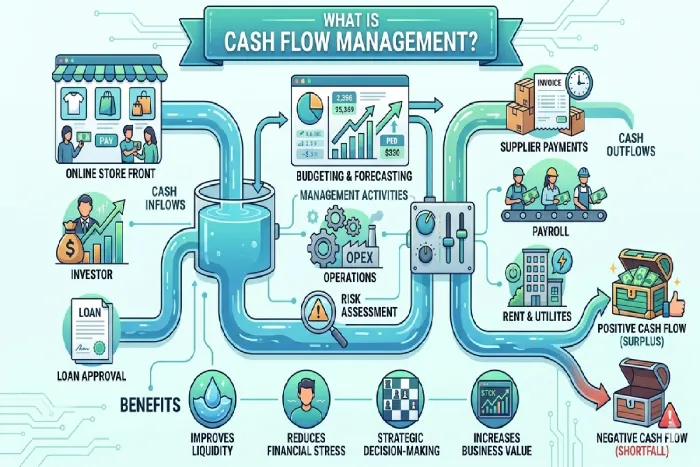

Managing cash flow encompasses forecasting, analysing, and monitoring a company’s inflow and outflow of cash. Do not confuse cash flow with net profit:

| Factor | Cash Flow | Profit |

| Definition | Real-time money coming in and going out | Revenue minus expenses over a period (on paper) |

| Reflects | Liquidity & ability to meet short-term obligations | Long-term financial performance |

| Measured by | Cash Flow Statement | Profit & Loss Statement |

| Timing | Immediate (payment delays hurt instantly) | Period-based (quarter/year) |

| Example | MSME selling online but facing UPI settlement delays | Startup showing profit post-funding but no cash for vendors |

Common Cash Flow Problems Small Businesses Face in 2026

Based on 2026 data from U.S. Bank, CNBC, and Indian MSME reports, here are the top 5 cash flow challenges:

1. Late Payments from Customers (Most Common)

- 49% of small business invoices are paid late

- Average B2B invoice in the U.S. is paid 8 days late; Indian SMEs wait 20–30 days beyond terms

- $825 billion in outstanding invoices owed to small businesses in the U.S. at any time

- Small businesses spend 14 hours/week chasing late payments

2. Unexpected Expenses

- 45% of survey respondents also list ‘unexpected operating expenses’ as a cause of their greatest cash flow gap.

- Equipment failure, changes in regulation, or loss of a critical employee can drain reserves quickly

3. Rapid Growth Without Sufficient Capital (“Growth Trap”)

- Growth uses up cash before it makes it;

- Starting new leases, employing employees or stocking inventory too early can leave perilous cash gaps

4. Seasonal Revenue Patterns

| Industry | Peak Season | Off-Season Revenue Drop | Common Financing Tool |

| Retail | Oct–Jan | 30–60% | Inventory financing |

| Landscaping | Apr–Oct | 50–80% | Working capital loans |

| Construction | Spring–Fall | 30–50% | Construction line of credit |

| Hospitality | Summer/Holidays | 40–70% | Short-term loans |

5. Inventory Management Inefficiencies

- Retail businesses report inventory as 60–80% of cash outflows

- Holding too much ties up cash; holding too little risks lost sales

Best Practices for Managing Business Cash Flow

1. Build a 13-Week Rolling Cash Flow Forecast

This is the gold standard for small business cash management, used by most fractional CFOs:

How to build it:

- Start with your current cash balance (actual bank balance today)

- Map expected inflows week-by-week (customer payments based on actual expected payment dates, not invoice dates)

- Map expected outflows week-by-week (payroll, rent, vendors, taxes, insurance)

- Calculate net cash flow for each week (inflows − outflows)

- Roll it forward weekly: drop the oldest week, add a new week, update based on actuals vs. projections

A negative number in any week is a warning signal. The power isn’t predicting perfectly—it’s giving you 6 weeks of lead time to accelerate collections, defer spending, or arrange credit.

2. Tighten Invoicing & Collections

- Invoice the same day you deliver work/product

- Set clear payment terms upfront and enforce consistently

- Automate payment reminders

- Offer 1–2% early payment discount for payment within 10 days

- Accept credit cards, ACH, and online payments

- Businesses that automate accounts receivable speed up invoice cycles by 60%

3. Renegotiate Vendor Terms

- Call your top 5 vendors and ask for better terms (Net 30 → Net 45 or Net 60)

- Ask about early payment discounts (2–3% off for payment within 10 days)

4. Build a Rolling Cash Reserve

- Target: 3–6 months of operating expenses

- Average small business holds only 60 days (2 months)

- Start by allocating a fixed % of monthly revenue to a separate account

- For seasonal businesses: 3–4 months recommended

5. Audit Recurring Expenses Quarterly

- Review every subscription, software license, insurance policy, and service contract

- Most businesses have hundreds to thousands/month going to unused tools

6. Align Growth Spending with Cash Cycle

- Before hiring, buying equipment, or marketing: model against your cash flow forecast

- Know when cash goes out, when you expect return, and what happens in the gap

Tools to Monitor Cash Flow Effectively (2026 Comparison)

| Tool | Best For | Key Features | Price (2026) |

| QuickBooks | Legacy users, accounting + cash flow | Cash flow planners, banking integrations | $30–$180/month |

| Float | Forecasting, QuickBooks/Xero integration | Scenario planning, graphical dashboards | $49–$229/month |

| CredFlow | Indian SMEs, receivables tracking | Invoice-based forecasting, real-time tracking | Free–₹2,999/month |

| Zoho Books | GST-compliant accounting (India) | Cash flow reporting, GST-ready books | Free–₹1,500/month |

| Pulse | Multi-currency, scenario planning | Graphical dashboards, budgeting | $29–$199/month |

| Tally Prime | Indian businesses, GST compliance | Visual receivables/payables dashboards | ₹13,500/year |

| Numeric | Real-time reconciled cash data | Auto-reconciliation, 13-week forecasts | $99–$499/month |

AI-Based Cash Flow Analysis is emerging in 2026: modern fintech systems identify unplanned expenses, cash shortages, and late payments automatically.

How Positive Cash Flow Supports Growth

Positive cash flow isn’t just about survival—it’s your growth engine:

| Benefit | Impact |

| Hire confidently | Pay payroll before client payments arrive |

| Invest in inventory | Stock up for peak season without depleting reserves |

| Seize opportunities | Respond to bulk purchasing discounts or new contracts |

| Negotiate better terms | Strong cash position = leverage with vendors |

| Avoid emergency financing | Proactive borrowers pay 20–40% less than reactive ones |

Key insight: Businesses with access to credit lines report significantly higher survival rates than those relying solely on internal cash.

FAQ Section

What is cash flow management?

Cash flow management assists companies in managing incoming and outgoing cash; monitoring, forecasting, and controlling it.

What are the 4 types of cash flows?

Earnings before interest and taxes; after deduction of tax; operating, investing, financing and free cash flow.

Why do we want to get rid of low cash flow?

It hampers bill settlement, salary payments, & emergency.

82% of small businesses fail because they have cash flow problems. Do?

Yes, the U.S. Bank research goes in depth, breaking down the hows and whys of the 82% that fail due to cash flow mismanagement.

What is the flow of cash?

Cash Flow = Cash Inflows – Cash Outflows

Final Thoughts: Cash Flow Management

Those businesses that succeed in maintaining a healthy cash flow aren‘t necessarily those with the highest revenues or best margins. Instead, they‘re those that have recognised the discipline involved in cash flow management, such as:

- Look at weekly reviews

- Discuss payment terms honestly with clients/vendors

- Build reserves when times are good

- Know when to escalate to fractional CFO expertise

Your business needs cash to survive because the time in between buying and collecting is what matters. Managing cash flow efficiently is perhaps the single most powerful action you can take as a business owner.