")

15 Financial Tips Every Small Business Owner Needs (2026)

Last Updated: July 17, 2026

Financial Tips are direct actions you can take to manage, build, and preserve your financial health. Examples of simple financial tips include setting up a budget to help understand how much money you earn and spend; working to reduce any debt with high interest; putting money aside to build an emergency fund that can cover between three and six months’ worth of expenses; and commencing contributions to retirement or superannuation funds.

What are Tips in Finance?

A tip in finance is a small sum of money that is given to somebody for services they have provided.

TIPS, in finance, is an abbreviation for Treasury Inflation-Protected Securities. These are bonds issued by the US government that serve to protect investors from inflation. As the cost of living goes up, your TIPS bond also increases in value.

How TIPS Work

Unlike a conventional bond, which pays a fixed interest rate on a fixed principal amount, TIPS have a face value that is linked to the CPI (Consumer Price Index).

- If inflation does happen, the principal of the bond increases.

- In the event of deflation, the amount is reduced, but you will receive back at least your original principal.

- Interest Payments: This fixed rate is used but on the now increased principal. This means as inflation increases, your interest payments are also increasing.

Key Details

- Maturity Terms: issued in 5, 10, 30 Jahren.

- About buying: U. S. Treasury securities are directly purchasable on the official platform of the U. S. Treasury, TreasuryDirect, or indirectly through mutual funds and ETFs.

- Risk and Return: Backed by the US government, they carry virtually no credit risk. As a result, they tend to have a lower initial yield than “vanilla” Treasuries, given their inflation protection.

15 Financial Tips Every Small Business

15 essential money tips that all small business owners should be trying to apply in 2026. They are grouped underneath your top five themes: cash flow, budgeting, expenses, taxes, and reserve fund.

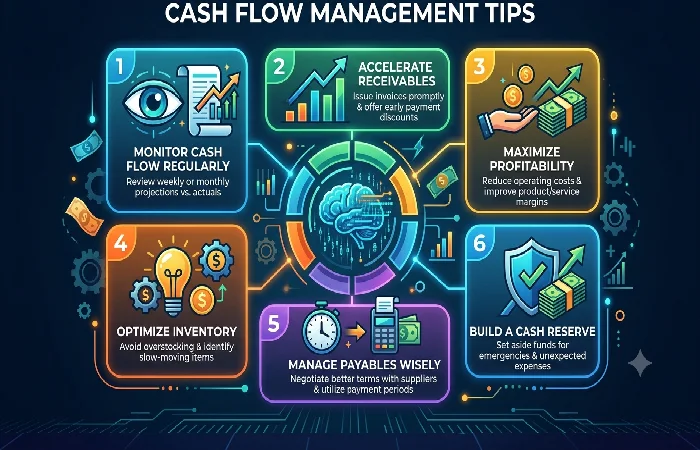

1. Cash flow management tips

- Monitor cash flow weekly, not just monthly, with a straightforward dashboard that shows cash inflow, cash outflow and overall position. Early warning signs, such as excess cash in or out, can alert you to potential difficulties.

- Maintain a minimum of 3–6 months’ worth of operating expenses in cash or highly liquid assets in order to prepare for slow seasons or shocks.

- Increase the collection of receivables by including shorter time limits, utilize internet based invoicing practices, and providing small incentives for quicker payments.

- Slow payables strategically utilize extended payment terms (e.g., 30 days), when possible, with suppliers without harming supplier relations, and only pay noncritical invoices early if able.

- Periodically analyze your cash flow statement so you will understand how cash is actually flowing through the business, not just your book profit.

2. Small Business Budgeting Tips

- Construct an annual budget and then divide it into monthly sales/revenue, expense, and profit targets; treat it as a living document and post and update it quarterly.

- Break down costs into must-have (software, rent, payroll) and nice-to-have (best business tools, marketing that isn’t essential to the business).

- Compare actuals vs. budget monthly to identify drift early; if revenue is below plan, change spending fast so you don’t rely on next month’s income.

- Apply easy ratios, like operating expenses as a percent of revenue, to observe if your cost structure is headed in a worthwhile direction over time.

3. How to Reduce Business Expenses

- Review all subscriptions and all agreed recurring charges at least twice a year, cancelling obsolete tooling and downgrading tiers where more functionality is purchased than used.

- Negotiate with vendors and landlords; most can be flexible given the right information and request. They will be happy to negotiate for better rates or discounts if you commit to longer terms or buy in bulk.

- Automate tedious tasks (bookkeeping, invoicing, reporting) to minimise admin hours and sensitivity to an edge case, reduction in potential headcount (direct or indirect). Use appropriate digital tools.

- Put more effort into efficiency gains (better processes, training, updated computer programs) that reduce your cost per unit produced, rather than just reducing obvious costs.

4. Small Business Tax Tips

- Make sure the bookkeeping is maintained accurately and monitored regularly throughout the year so you have time to plan for tax, instead of rushing to do at the last minute; tidy accounts reduce errors, and deductions can be claimed.

- Consult with a tax accountant to find out what deductions, credits and incentives are available in your jurisdiction (e.g., depreciation rules, R&D credits, local GST/VAT intricacies) and how to efficiently plan the timing of income and expenses.

They include: having separate banking accounts for the business and personal life (and having one credit card for each); building up credit image for the business over a period of time; and always rethinking whether your entity formation model continues to be a viable structure in terms of taxation and liability protection.

5. Business Emergency Fund

A business emergency fund a reserve of cash (or other ready asset) intended to sustain 3–6 months of essential expenses (e.g., rent, payroll, software, loan payments) in case revenue suddenly falls below projections.

How do I do this? Make the monthly “emergency fund contributions” line item a non-negotiable expense in your budget. Set up an auto-transfer to a separate account that is not used for growth projects, and don‘t touch the money. It‘s there just to keep your business alive through shocks.

Conclusion

Effective financial management is a key factor in the growth and survival of small businesses rather than stagnation and failure. When 2026 arrives, you will have a far better chance to succeed with effective cash flow management, setting a realistic budget, reducing unnecessary expenses, projecting tax payments, and preparing a contingency. Your business will be better prepared to deal with uncertainty and better positioned to take advantage of opportunity.

All your systematization in the areas of income, expense, profit, and shockproofing directly help you to focus on and manage marketing, sales and, growth rather than always playing catch-up.

FAQs

Q1. How frequently should cash flow be reviewed in a small business?

You should check cash flow at least weekly, with a more detailed review once a month. If you check weekly, you can catch short-term problems (e.g. customers paying late) early. Monthly reviews can identify trends and seasonality.

Q2. How are profit and cash flow different from each other?

Profit what you actually make on paper after income minus costs. Cash flow the movement of money both in and out of your bank accounts. You can be profitable and still be struggling if cash is ‘locked’ in unpaid invoices and stock.

Q4. Is a formal, detailed budget necessary in a small business?

Yes. Even a basic rolling annual budget divided into monthly indicators provides some guardrails around your expenditure and a starting point for measurement. If you don’t have a budget, you’ll never be sure the excesses are anomalies or entrenched.

Q5 How precise should the budget be?

Spreadsheets should at the very least distinguish between revenue, fixed costs(rent, salaries, insurance), variable costs (marketing, transaction fees, commissions) and planned investments. They should be detailed enough to understand your sources of variation, but not so detailed you just stop using it.

Q6 Define a business emergency.

Emergencies are things that have to be dealt with immediately, such as revenue loss. The sudden loss of a large customer, unforeseen legal or regulatory expense, or equipment failure. Or probably the most frightening of them all, sudden economic shock. Opportunities (e.g., a successful advertising test, expansion or acquisition) are not emergencies and are to be funded separately.