Personal Finance Tips Every Business Owner Should Know

Last Updated: June 23, 2026

The business-owning ‘how-to’ tips for personal finance that each business owner needs to adhere to are starkly different from simple personal budgeting advice. In 2026, with 33% of all U. S. Adult are planning to start a business (a 94% increase from the previous year) and cash flow surpassing inflation as the No.1 operational challenge for 40.8% of all business owners, understanding the blending of personal finances and business finances has become more imperative.

As someone who’s sat on both sides, advising dozens of startups literally and living on a razor blade between personal bills and business expenses, I’m convinced that separating your personal assets from your working assets isn’t just the right thing to do; it’s the only thing to do. This is an all-in-one pruning shears of a treasure chest loaded with over 5 years of 2026-researched, proven, practical strategies to build financial permanence.

| Intent Type | What You’re Looking For | What This Article Delivers |

| Informational | How to separate personal/business finances, emergency fund amounts, tax strategies | Step-by-step guides with 2026 data jpmorgan+1 |

| Commercial | Best financial tools, advisor services, funding options | Product comparisons and professional guidance recommendations jpmorgan+1 |

Businesses such as J. P. Morgan and AMBA-BGA mention the important role of pre-startup planning, but fail to address those maintenance strategies that advanced business owners are crying for.

1. Separate Personal and Business Finances

The data: 80.8% of business owners do their own taxes, and doing too many things (i.e., mixing business and personal finances) is the top mistake that makes doing them even harder.

Why This Matters in 2026

When you blur personal and business finances:

- Tax deductions become unauditable

- Business cash flow problems ruin personal credit

- Investors are unable to determine how well your business has truly performed financially:

- Legal liability protection(LLC/corporate veil) becomes jeopardized

How to Do It Right

Step1: Separate business banking accounts.

- Business checking for everyday business activities.

- Business savings for taxes and emergency reserves.

- Personal checking for your salary/distributions.

Step 2: Obtain specific Business credit cards.

- Establish business credit on your own.

- Use accounting software to automatically keep track of expenses

- Do not use personal cards for your expenses.

Step 3. Pay yourself a salary.

- Maintain a fixed payroll schedule.

- Treat yourself like you would any other employee.

- Adjust depending on the Company‘s cash flow.

2. Build Multiple Emergency Funds (Personal + Business)

The 2026 picture: cash flow and access to capital are identified as the top most challenge for 40.8% of all business owners; 17% of all business owners reduce their own wages to preserve cash flow.

The Dual Emergency Fund Strategy

| Fund Type | Target Amount | Where to Keep It | Purpose |

| Personal Emergency Fund | 6-12 months of living expenses | High-yield savings account | Cover personal bills if business income stops |

| Business Emergency Fund | 3-6 months of operating expenses | Business savings account (separate from operating) | Pay employees, rent, suppliers during revenue dips |

| Tax Reserve Fund | 25-30% of all income received | Separate business savings | Quarterly tax payments without cash flow stress |

2026 Data Insight

According to the Guidant Financial 2026 survey, 17% of business owners lowered their own wages to maintain cash flow and 56.2% responded to inflation by raising prices. The presence of predetermined emergency funds avoids when they respond.

Personal record why 6-12 months? As 33.3% of companies will have lost during 2026 and only 57.5% of companies are profitable at the moment

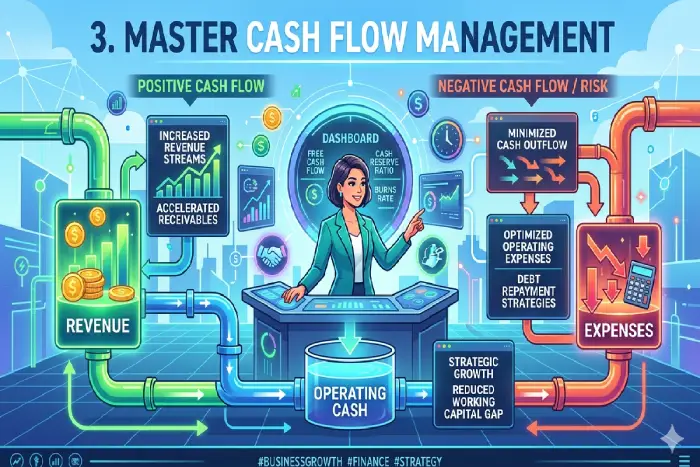

3. Master Cash Flow Management

Critical insight: Cash flow is one of the most critical concerns for any business and it‘s now the #1 concern for 40.8% of owners, surpassing inflation.

The Cash Flow vs. Profit Gap

Many business owners make the fatal mistake of confusing profit with cash flow:

You can make a profit on paper but then go bankrupt because your customers haven‘t paid you yet.

Weekly Cash Flow Routine

- Monday: Check on your (who you owe money) Accounts Receivable

- Wednesday: Review your Accounts Payable (who you owe)

- Friday: Schedule 30 days cash flow projection during project.

Tools that help in 2026:

- QuickBooks (used by over 60% of entrepreneurs with AI integration)

- FreshBooks for service-based companies

- Xero for e-commerce

4. Invest Strategically (Personal + Business)

2026 trend: household ownership of equities increased in India to 18.8% in Sept 2025. Equity/Mutual Funds comprised 15.2% of annual savings (compared to 2% in FY12).

Investment Planning for Business Owners: The Three-Bucket Approach

1: Personal Retirement (Tax-Advantaged First)

- Maximum out 401(k)/NPS/PPF contributions

- IRA/SIP investments in index funds

- Never cash out retirement plans to fund the business. (96.5% of business owners who used a ROBS successfully if they cashed out a retirement plan)

2: Business Growth Investments

- Reinvest 20-30% of sales revenue within the business.

- AI tools (18.7% of owners proposing AI investment in 2026)

- Digital marketing (38.6% are increasing this budget)

3: Personal Wealth Building

- There is a diversified stock portfolio (other than in his own business)

- Real estate on if cash flow can support it

- Objective: Never have in excess of 50% of net worth in your business.

2026 Wealth Management Data

In the Fiscal Year 2026 Economic Survey, 2026: It reports that the share of equity and mutual funds in total household financial assets increased to 23% from 15.7% in 2019 and the share of deposits in total household financial assets declined to 35% from 58%.

| Investment Vehicle | 2026 Allocation Recommendation | Risk Level |

| Index Funds/ETFs | 40-50% of personal portfolio | Medium |

| Direct Equity | 20-30% (if experienced) | High |

| Real Estate | 15-20% | Medium-Low |

| Fixed Deposits/Bonds | 10-15% | Low |

| Business Reinvestment | 20-30% of profits | Variable |

5. Personal Budgeting Tips Specific to Business Owners

The problem: 52% of potential entrepreneurs are not confident in managing cash flow and taxes

The 50/30/20 Rule Doesn’t Work for Business Owners

Standard personal budgeting fails because business income fluctuates. Use this instead

The “Safe Salary” Budgeting Method

- Calculate your lowest monthly requirements (rent, food, utilities, loans, etc.)

- Always pay yourself the same amount from the business no matter how much money you earn.

- Build up personal surplus for the 4 months of higher income from various sources

- Use surplus to raise salary step by step instead of doing it in low months.

Budget Breakdown for Business Owners

| Category | Percentage of Personal Income | Notes |

| Needs | 40-50% | Rent, groceries, insurance, minimum debt payments |

| Wants | 15-20% | Entertainment, dining, hobbies (cut first during downturns) |

| Savings/Investments | 25-30% | Emergency fund, retirement, taxable investments |

| Business Reinvestment | 10-15% | Personal time spent on business education, networking |

2026 Reality Check: Americans think they need $28,000 to start a business, but the true median cost is only $12,000. Don’t let perceived costs inhibit your ability to develop an appropriate personal reserve fund.

6. Entrepreneur Financial Planning: The 5-Year View

The shift: 18.2% of entrepreneurs are driven by legacy-building thinking past exit to generations of wealth.

Investment Planning for Business Owners by Stage

Year 1-2: Survival Mode

- Priority: (emergency fund personal (6-12 months))

- Business: Build cash reserves (aim for 3 months of operating costs)

- Investment: Maximum tax-advantaged accounts only.

- Objective: Not going bankrupt.

3-5Year: Stability Mode

- Focus: Raise salary to market standard; appropriate in relation to the other team members and the use of the programs.

- Business: Invest in systems (AI, automation)

- Investment:20% in diversified portfolio

- Goal: Establish personal wealth separately from business.

Year 5+: Growth Mode

- Focus: Estate planning, succession

- Business: Scale or prepare for exit

- Investment: 30%+ to wealth building

- Goal: Multi-generational wealth

2026 Exit Planning Data

12.8% of business owners are planning to sell in 2026 (compared to 11.0% in 2025). This forms a budding wave of business disruption.

FAQ Section

How much savings should business owners build up?

A: 6-12 months of personal expenses in a high-yield savings account. This cushion is critical as 33.3% of businesses expect to see revenue decrease in 2026 with only 57.5% profitable.

Is starting a business worth using my 401(k)?

Answer: Only with ROBS structure– 96.5% of all successful funded companies use the same. Never take early (penalties + lost compounding growth).

What are the best investments for entrepreneurs?

Diversify: 40-50% index funds, 20-30% direct equity if you are experienced, 15-20% real estate, 10-15% bonds. Never allocate over 50% of your net worth to your business.